.

.

1. When?

From 1 July 2021.

.

2. Who will be affected?

– online retailers (both EU and non-EU) who sell goods or services to EU consumers;

– electronic interfaces (online platforms and marketplaces) which facilitate B2C sales to European Union consumers.

.

3. Main changes

All B2C supplies to EU customers will be taxed at destination

Their origin (either EU or non-EU) will matter no more. The retailers can still be registered in all EU member states to which they supply or they can use one of the schemes (union or import) for simplification of the process of collecting and reporting VAT.

Distance selling VAT threshold regime is being changed

From July businesses will have to apply VAT when their cross-border B2C sales exceed EUR 10,000. However, retailers can close their VAT registrations in the EU member states and declare VAT in one member state using the One-Stop Shop scheme.

The EUR 22 VAT exemption for imports will be abolished

All import goods will be subject to VAT. However, for import goods valued EUR 150 or less, retailers will be able to charge VAT at the point of sale (rather than collected from the receiver) using the new EU import scheme – Import One-Stop Shop.

Online platforms marketplaces will collect VAT instead of their sellers

The electronic interfaces will be responsible for collecting and reporting VAT for B2C transactions rather than their sellers in 2 cases: if the consignment which is dispatched from a third territory is valued less than EUR 150, or if non-EU retailers sell goods (of any value) located in the EU. It means that retailers making such transactions using online marketplaces will no longer need to be registered in EU member states

.

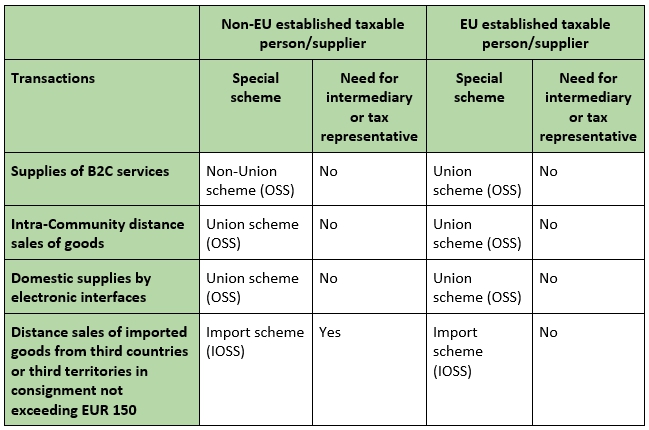

4. New special schemes (OSS and IOSS)

The new rules will modify existing union and non-union schemes and will add a new one – import scheme. General information about all the amendments is presented in the table below:

Table 1. Overview of changes to the special schemes as of 1 July 2021

(data taken from https://ec.europa.eu/)

Reporting in any scheme (whether it is OSS or IOSS) is voluntary. The tax period for OSS will be quarterly, for IOSS monthly.

.

4.1 OSS (One-Stop Shop

Non-Union scheme.

| Scope until July, 1: Applied only to telecommunications, broadcasting and electronic (TBE) services | Scope after July, 1: All services including TBE |

The non-Union OSS:

- can be applied to B2C services only;

- can be used by non-EU retailers only.

The scheme allows businesses to declare and pay in one EU member state via One-Stop Shop (OSS, non-union scheme) instead of registering in each member state to which they supply their services.

Union scheme.

| Scope until July, 1:

Applied only to telecommunications, broadcasting and electronic (TBE) services Distance selling thresholds – EUR 35 000 or 100 000, depending on the member state | Scope after July, 1:

All services including TBE EU-wide threshold of EUR 10 000 per annum |

New threshold in distance sales means that below EUR 10 000 businesses can still continue to apply the domestic rules for VAT on B2C cross-border sales. But if the sales are above this threshold, retailers will have 2 opportunities:

- to register for VAT in all EU member states where they supply to and pay and report VAT according to the rules of those member states; or

- to register in One-Stop Shop (OSS, unione scheme) and report VAT through a tax portal of one member state.

The union OSS:

- can be used by non-EU retailers for distance sales of goods to EU customers;

- can be used by EU retailers for supplies of any services and distance sales to member states in which they are not established;

- can be used by online platforms and marketplaces for distance sales of goods within the EU and certain domestic supplies of goods.

.

4.2 Import scheme (IOSS)

| Scope until July, 1:

No import VAT has to be paid for goods of a value up to EUR 22 | Scope after July, 1:

All import goods are subject to VAT irrespective to their value |

The Import One-Stop Shop (IOSS):

- can be applied to imported goods only;

- can be used for consignments not exceeding EUR 150.

New IOSS scheme allows businesses to charge VAT at the point of sale. But goods subject to excise duty (such as alcohol and tobacco products) are excluded. This will allow your customers to pay the final price, without hidden charges or fees. Otherwise the customers will pay VAT upon importation of goods in the EU and they may also need to pay couriers or postal operators charges.

If the supplier is not established in the EU and not established in a third country with which the EU has concluded a VAT mutual assistance agreement, then such a supplier is obliged to have a EU-based intermediary to fulfil their VAT obligations under IOSS.

.

5. How to register

The electronic registration for the OSS (Union scheme) or IOSS via the tax administration’s portal is open from April 1st.

If a business is established in the EU it is required to register in the member state of establishment.

If a non-business has fixed establishments in one or more EU member states, it must register in one of them.

If a business has no fixed establishment within the EU, it can choose in which country to register.